When you order generic medications from an online pharmacy, your insurance might cover it - or it might not. It’s not as simple as just clicking "buy" and expecting your plan to pay. Many people assume that if a drug is generic and sold online, insurance will treat it like a regular pharmacy. That’s not always true. In fact, the difference between a mail-order pharmacy tied to your insurance and an independent online retailer can mean the difference between paying $5 or $200 for the same pill.

How Insurance Actually Covers Generics

Your health plan doesn’t just pay for any generic drug you find online. It has a formulary - a list of approved medications - and divides them into tiers. Generics are almost always in Tier 1, the cheapest. That means your out-of-pocket cost is usually a flat copay: $5 for a 30-day supply, $10 for 90 days. But this only applies if you use a pharmacy in your plan’s network. Pharmacy benefit managers (PBMs) like CVS Caremark, Express Scripts, and Optum Rx run these networks. They negotiate prices with drugmakers and set the rules. When you fill a prescription at a retail pharmacy or through mail-order, the system checks your insurance ID against the formulary in real time. If the drug is covered and the pharmacy is in-network, your copay is locked in. If not? You pay full price.Mail-Order vs. Independent Online Pharmacies

Not all online pharmacies are the same. There’s a big difference between:- Mail-order pharmacies - these are part of your insurance plan’s network. You get prescriptions filled by mail, often for 90-day supplies. They usually have lower copays than retail - $10 for 90 days of metformin, for example.

- Independent online pharmacies - these are like Amazon or Walmart’s online drug service. They may accept insurance, but only if they’re in your plan’s network. Many aren’t. If you order from one that’s out-of-network, your insurance won’t cover it. You’ll pay full price upfront and then file a claim for partial reimbursement - if your plan even allows it.

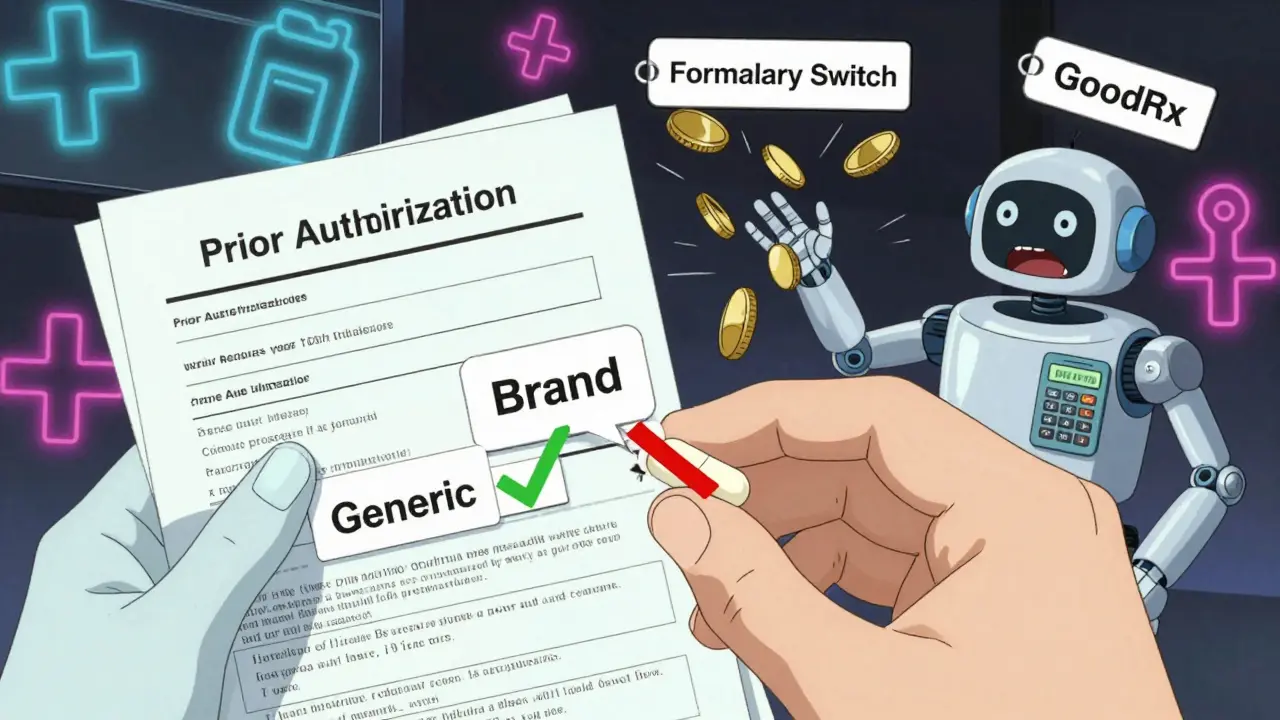

GoodRx and other price-comparison tools show that sometimes, even without insurance, you can pay less at a big-box retailer like Walmart than your insurance copay. Their $10 for 90-day generic program covers dozens of common meds. For people with high-deductible plans, that’s often the better deal.

What Happens When Your Insurance Switches Your Drug

You might wake up one day to find your brand-name medication replaced with a generic - without your doctor’s input. This is called non-medical switching. Insurers do it to save money. If a generic version exists, they’ll push it onto you, even if your doctor prescribed the brand. This isn’t just paperwork. One patient with multiple sclerosis reported severe side effects after her insurance switched her from Copaxone to a generic without warning. She ended up in the ER. While generics are bioequivalent, some people react differently to inactive ingredients or manufacturing processes. You have rights. If a switch causes problems, your doctor can file a formulary exception or prior authorization. This means they submit medical evidence - your history, side effects, test results - to ask for the brand to be covered. Many patients don’t know this is an option. But it’s built into most plans.

Amazon RxPass and Other New Models

Amazon Pharmacy’s RxPass is changing the game. For $5 a month, Prime members get unlimited access to over 100 generic medications. No copays. No insurance needed. It’s a flat fee - like Netflix for pills. It’s not a replacement for insurance. It’s an alternative. If your deductible is $6,000 and you’re paying $15 per prescription, RxPass saves you money fast. But it doesn’t cover everything. Thyroid meds, certain antibiotics, and specialty generics are often left out. And you need to be a Prime member. Other services like Honeybee Health are trying similar models - direct-to-consumer pricing without insurance middlemen. These are still small, covering less than 2% of the generic market. But they’re growing fast.How to Check Coverage Before You Order

Don’t guess. Here’s how to know for sure:- Find your insurance plan’s formulary. Most insurers have a searchable tool on their website. Type in the first three letters of your drug name - for example, "lis" for lisinopril.

- Check if your pharmacy is in-network. If you’re ordering from an online pharmacy, call them. Ask: "Do you accept my insurance plan?" Give them your plan name and member ID.

- Compare prices. Use GoodRx or SingleCare. Sometimes the cash price is cheaper than your copay. Especially if you’re still paying your deductible.

- For maintenance drugs (blood pressure, diabetes, cholesterol), ask your doctor for a 90-day prescription. Mail-order often saves money here.

Some plans even let you check your exact cost before you fill a prescription through their member portal. It shows real-time pricing based on your deductible, coinsurance, and pharmacy choice.

What to Do If You’re Charged Wrong

You paid at an online pharmacy and your insurance didn’t cover it? Here’s what to do:- Check if the pharmacy is in-network. If it’s not, your insurer won’t pay - and you shouldn’t expect them to.

- Save your receipt. If your plan allows out-of-network reimbursement, submit a claim with the receipt and prescription details.

- Contact your insurer’s pharmacy help line. Most have a 24/7 nurse line. For example, MHBP’s number is 1-800-556-1555. Ask: "Why wasn’t this covered?" They can explain your formulary rules.

- If you were switched to a generic without notice and had side effects, ask for a formulary exception. Your doctor can help.

According to insurer data, nearly 27% of calls to customer service involve confusion about generic substitution. You’re not alone.

What’s Changing in 2026

The landscape is shifting fast. By 2025, over 45% of generic maintenance drugs will be delivered by mail or home delivery - up from 32% in 2022. PBMs are expanding "generic-only" tiers, meaning more drugs will be restricted to generics, even if your doctor prefers the brand. Twenty-eight states now cap out-of-pocket costs for generics at $15-$20 per prescription. The federal government is also pushing for more price transparency. And with the Medicare Drug Price Negotiation Program rolling out, commercial insurers are starting to mirror those price caps. Amazon RxPass and similar services aren’t replacing insurance yet. But they’re forcing PBMs to adapt. Expect more flat-fee models, more direct pricing, and more pressure to cut out the middleman.If you’re on a chronic medication, the smart move is to compare your options every few months. Your insurance plan changes. Your pharmacy network changes. Your costs change. The best deal today might not be the best next year.

Do all online pharmacies accept my insurance?

No. Only pharmacies in your insurance plan’s network will accept it. Many independent online pharmacies are out-of-network. Always call the pharmacy and give them your insurance ID before ordering. If they say they don’t accept your plan, you’ll pay full price and may need to file a claim for partial reimbursement.

Is it cheaper to use insurance or pay cash for generics?

It depends. For people with high-deductible plans, paying cash at Walmart or Costco can be cheaper than your copay. A 90-day supply of metformin might cost $10 cash but $15 with insurance if you haven’t met your deductible. Use tools like GoodRx to compare cash prices with your insurance copay before deciding.

Can my insurance force me to switch from a brand drug to a generic?

Yes. This is called non-medical switching. Insurers do it to cut costs. If a generic version exists, they’ll require you to use it - even if your doctor prescribed the brand. If you have side effects or medical reasons to stay on the brand, your doctor can file a prior authorization or formulary exception to override the change.

What’s the difference between mail-order and online pharmacy?

Mail-order pharmacies are part of your insurance network - they’re run by your PBM (like Express Scripts) and require 90-day prescriptions. Independent online pharmacies (like Amazon Pharmacy) may or may not be in-network. Mail-order often has lower copays but takes a week to arrive. Independent pharmacies might offer faster shipping but may not accept your insurance at all.

Does Amazon RxPass replace insurance?

No. RxPass is a flat $5/month subscription for over 100 generics - no insurance needed. It’s a good option if you’re on a high-deductible plan or if your insurance doesn’t cover your specific medication. But it doesn’t cover all drugs, and you need to be a Prime member. It’s an alternative, not a replacement.

How do I know if a drug is covered by my plan?

Go to your insurer’s website and use their drug lookup tool. Enter the first three letters of the drug name. It will show you the tier, your copay, and whether it’s covered. If you’re unsure, call your insurer’s pharmacy help line. Most have a 24/7 nurse line ready to answer.

Why does my insurance cover some generics but not others?

Your plan’s formulary decides which generics are covered - not all generics are the same. Some are preferred (lower cost), others are non-preferred (higher cost or not covered). This is based on negotiations between your PBM and drugmakers. Even two versions of the same drug can have different coverage rules.

Wow, this is actually one of the most clear breakdowns I’ve seen on how insurance handles generics. I used to think if it was generic, it was covered - until I got stuck with a $180 bill for metformin because I ordered from some random site. Turned out Walmart had it for $10 cash. Sometimes the system is just designed to confuse you.

Now I check GoodRx before I even open my insurance portal. It’s saved me hundreds. Also, 90-day mail-order? Game changer if you’re on a chronic med. Just make sure your pharmacy’s in-network - call them. Don’t assume.

Why are we still pretending insurance works? It’s a labyrinth of middlemen. PBMs aren’t saving you money - they’re siphoning it. Your $5 copay? That’s after they negotiated a 700% markup with the manufacturer. The real savings are on cash at Costco or Amazon RxPass. Insurance is just a tax you pay to play a rigged game.

My mom got switched to a generic for her blood pressure med last year and had a panic attack. Not because of the drug - because she didn’t know she could fight it. She called her doc, they filed a prior auth, and they let her keep the brand. No one told her this was an option. Please, if you’re reading this - ask your doctor about exceptions. You’ve got rights. Don’t let them push you around.

OH MY GOD. I CAN’T BELIEVE YOU ACTUALLY THOUGHT THIS WAS COMPLICATED??

IT’S SIMPLE. IF YOU’RE USING A NON-NETWORK PHARMACY, YOU’RE PAYING FULL PRICE. PERIOD. YOU DON’T GET A PASS BECAUSE YOU ‘DIDN’T KNOW.’

YOUR INSURANCE PLAN ISN’T A MYSTERY - IT’S A DOCUMENT. YOU HAVE A MEMBER PORTAL. YOU HAVE A PHONE NUMBER. YOU HAVE A 24/7 NURSE LINE. YOU DON’T NEED A PHD TO CALL AND ASK. YOU JUST NEED TO BE RESPONSIBLE.

AND DON’T EVEN GET ME STARTED ON AMAZON RXPASS. IT’S NOT A ‘NEW MODEL’ - IT’S THE ONLY SENSIBLE ONE. WHY ARE WE STILL USING PBMs TO PLAY GUESS-THE-COPAY WHEN YOU CAN JUST PAY $5 A MONTH AND BE DONE WITH IT?

WE’RE LIVING IN 2025. STOP ACTING LIKE THIS IS 2007.

They’re not telling you this, but PBMs are in bed with big pharma. The ‘generic’ you get isn’t always the same as the one at Walmart. Different fillers. Different binders. Sometimes it’s the same molecule, sometimes it’s a knockoff with a different manufacturer code.

And the reason they push mail-order? Because they get kickbacks from the mail-order companies. You think you’re saving money? You’re funding a cartel.

Amazon RxPass? Yeah, it’s great. But it’s also a Trojan horse. They’re building a healthcare monopoly under the guise of convenience. Next thing you know, your insulin is only available through Prime. And good luck canceling that subscription.

Oh wow, another ‘educational’ post from someone who thinks reading a formulary is activism. Let me guess - you also believe that ‘checking GoodRx’ is a radical act?

Here’s the truth: insurance doesn’t care about you. PBMs don’t care about you. The government doesn’t care about you. You’re a data point in a spreadsheet. The only thing that works is cash, direct payment, or going off-insurance entirely. Stop pretending the system is fixable. It’s not. It’s a Ponzi scheme with a pharmacy counter.

There is a deeper truth here. The pharmaceutical system is not broken - it was designed this way. The illusion of choice - insurance, mail-order, cash, RxPass - is merely a performance to distract from the central truth: health is commodified. We are not patients. We are consumers. And consumption, in this context, is a form of surrender.

When you compare $5 to $15, you are not choosing savings - you are choosing to participate in a system that values profit over person.

The real question is not how to pay less - but why we accept this as normal.

OMG YES I JUST HAD THIS HAPPEN 😭

I ordered my thyroid med from some ‘discount pharmacy’ because it said ‘insurance accepted’ - turned out it wasn’t in my network. Got charged $120. Filed a claim. Waited 6 weeks. Got $18 back. I’m still mad.

Now I only use Walmart’s $10 list or Amazon RxPass. No insurance hassle. No forms. No ‘you’re not covered.’ Just pay $5 and move on. I’m never trusting another online pharmacy again. 🤡

This is so scary. I just found out my insurance switched my diabetes med to a generic I’d never heard of - and now I’m having nightmares, dizziness, I can’t sleep. I went to the ER. They said it’s ‘possible’ the inactive ingredients are reacting with my body. I’m scared. What if this happens to someone with epilepsy? Or cancer? We’re being used as guinea pigs. No one told us. No one warned us. This isn’t healthcare - it’s a gamble. And I’m losing.

Interesting read. I’ve been using RxPass for six months now and it’s been great. I’m not anti-insurance - I just think there’s room for alternatives. The fact that we even have to debate whether a $5 monthly fee is better than a $15 copay says something about how broken the system is.

Maybe the real win isn’t choosing between insurance and cash - it’s pushing for a future where both are obsolete. Where meds are affordable by default. Not because we’re clever shoppers, but because we’ve fixed the root.

im in india and we dont have insurance but i get my meds from local pharmacy for like 200rs. i think this whole system is crazy. why does it cost so much in us? its the same pill. same chemistry. why? just because its usa? i dont get it.

While the emotional responses above are understandable, it’s important to recognize that the current system - despite its flaws - exists to balance cost containment, access, and regulatory compliance. The role of PBMs, formularies, and tiered coverage is not malicious - it’s structural, driven by market dynamics and legislative frameworks.

That said, consumer education, transparency tools, and alternative models like RxPass are legitimate pathways forward. The goal should be reform, not rejection. Patients deserve clarity - and increasingly, they’re getting it.